Frequently Asked Questions (FAQs)

If you have questions about your loan with RANLife Home Loans and would like to speak to someone, please call us at (877) 845-2854. Our Homeowner Care team members are available Monday – Friday 8:00 am – 9:00 pm ET and Saturday 8:00 am – 12:00 pm ET and our Ally department is available Monday – Friday 8:00 am – 9:00 pm ET.

Standard Servicing Fee Schedule

Accessibility & Language Access

Forbearance

What do I need to know about forbearance?

You should know that during a forbearance, no payments are expected; however, payments will still be accepted. There will be no late charges assessed to your account, and negative credit reporting is suppressed.

Important: If you are set up on recurring ACH payments, entering a forbearance plan will automatically turn off your recurring payments. If you would like to continue to make full or partial payments through recurring ACH, you will have to re-enroll in our auto drafting program.

The purpose of a forbearance is to offer temporary relief by suspending payments for a set period of time. However, it is important to understand that once the forbearance plan expires, the total amount of all outstanding monthly mortgage payments that were suspended during the forbearance period, as well as any previously delinquent amounts, will become due, unless further assistance is requested and addressed through post-forbearance options, and credit reporting will resume.

For example: Let’s say your monthly mortgage payment is $1,000, including principal, interest, taxes, and insurance. If you choose to enter a 90-day forbearance plan, you won’t owe that $1,000 for the next three months. But at the end of the 90-day plan, you’ll owe $3,000 (or $1,000/month for the past 3 months) to become current again.

This can result in payment shock for some, which is why as your servicer we will remain in contact with you during your forbearance period to discuss your unique situation, including what options are available to you for paying back the missed payments at the end of your forbearance term. Depending on your loan product and eligibility status, a variety of options may be available to you for short term or long-term relief.

Login to learn more about this option.

If you have an online account, you can log in to request a forbearance. One of our team members will review your request and give you a call back to discuss the terms and conditions. We want to make sure you fully understand the details of this program before signing up.

Why am I only being offered a 90-day forbearance? I am hearing I can get one for longer

CARES ACT and COVID-19 RELATED FORBEARANCES

While it is true that under the CARES Act forbearances can be offered for up to 180 days, and extended out for another 180 days, it’s important to understand that a forbearance effectively kicks payments “down the road”. When the forbearance period ends, you’re still obligated for all the missed payments. The longer the forbearance period, the more missed payments you’ll have to repay, which means a larger sum that will become due. That can create a tremendous financial burden, which may be too much for some to bear. If not handled responsibly it could ultimately lead to default, which could result in foreclosure.

That’s why we believe the best way to manage this program is to start with a 90-day forbearance period, which provides our homeowners with immediate payment relief to address the financial impact of the COVID-19 pandemic.

Prior to the initial 90-day relief period expiring, together we can assess your financial situation and work with you to determine which of the available post-forbearance options is best for you to help get you back on track. Depending on your loan product and eligibility status, a variety of options may be available to you for short term or long term relief.

What can I expect during the forbearance period?

During your forbearance period, no payments are expected. There will be no late charges assessed to your account, negative credit reporting is suppressed, and you will continue to receive your monthly billing statement. We will contact you to discuss your specific situation, including what options are available to you at the end of your forbearance term. If you have any questions, during your forbearance period, please contact us. We’re here to help you.

Can I make payments during my forbearance period?

Yes, you can make payments during your forbearance and we encourage you to do so if possible. Even if you can’t make your full monthly payment, partial payments will be accepted under forbearance plans. We will hold partial payments (payments that are less than your scheduled monthly payment) in a separate account until you pay the remainder of the payment. Upon receipt of enough funds to pay your full monthly payment, we will apply your full payment to your account, and your next payment due date will update accordingly.

It is important to remember that the forbearance plan is intended for temporary hardship, and is not intended for long-term relief. Once the forbearance plan expires, the total amount of all outstanding monthly mortgage payments that were suspended during the forbearance period, as well as any previously delinquent amounts, will become due. So if you can pay even part of your monthly obligation during the forbearance plan, we encourage you to do so, as it will reduce the total amount due at the end of your forbearance plan.

Important: If you are set up on recurring ACH payments, entering a forbearance plan will automatically turn off your recurring payments. If you would like to continue to make full or partial payments through recurring ACH, you will have to re-enroll in our auto drafting program.

If my situation changes, can I cancel my plan before the forbearance period ends?

Yes, you can cancel your forbearance plan at any time. Should your financial situation improve prior to the end of your forbearance period, and you are able to resume making your normal payments again, we can stop your forbearance plan and work with you on your options to get you back on track. Just remember that ending your forbearance plan will also end the protections of negative credit and late charge suppression.

How will forbearance impact my credit?

Through the duration of your forbearance plan, we will not assess any late charges and negative credit reporting will be suppressed, but only for the duration of the plan. Once your forbearance plan ends, we will resume credit reporting. Each credit bureau leverages their own algorithms to determine how to score your credit, and although negative credit reporting is suppressed during a forbearance, meaning we will not report that a payment was skipped during the forbearance plan, it is possible that a credit agency may assess your credit differently in the absence of such reporting. If you have questions on how credit bureaus measure credit scores, we encourage you to contact them directly.

Will this impact my ability to refinance in the future?

Remember that while you’re on a forbearance plan, we will not negatively report your credit. However, it’s possible that some lenders or loan products may restrict refinancing if you’ve recently been on a forbearance plan. If you have questions, we suggest you speak with your mortgage lender or a licensed mortgage loan originator regarding your ability to refinance.

What are my options after the forbearance period?

Before the end of your forbearance period, we will work together with you to determine what will be the appropriate next steps based on your unique situation. We ask that you contact us 30-days prior to the end of your forbearance plan, which gives us time to reassess your hardship and financial status, and helps us determine your eligibility for additional relief options. Some of those options include:

A reinstatement: This is where you make up missed payments in a lump sum to bring your account current and continue to make regular, on time payments. While that’s the quickest way to get back on track, we understand every situation is unique and not everyone will be able to do this. Rest assured that you have other options and a lump sum payment is not required unless you wish to do so.

A repayment plan: This is where you work to bring your loan current over time by making monthly payments in excess of your contractual payment amount.

A deferral or standalone partial claim: This is where the amount of the delinquency moves into a non-interest bearing balance, due and payable at maturity of the mortgage loan or earlier payoff. This option is not available for all loan products. In order to qualify certain criteria must be met.

An extension of your forbearance: If your situation has not changed, or is still unstable, you can request an extension of your forbearance for a longer period of time. But remember, any payments suspended during forbearance will still need to be paid back.

Loan modification: This is where we modify the terms of the Note to help get you current and potentially provide for a lower monthly payment going forward. In order to take advantage of this option, you’ll have to submit a full mortgage assistance application package for review.

Each of these options have their pros and cons, and may have additional eligibility and qualification requirements. That is why it is important that we stay in contact throughout your forbearance term so that we can work together to determine the right solution that’s tailored to your unique situation.

How do I know which option is right for me?

We`re here to help you get back on your feet. Contact us today or talk to a HUD-approved housing counselor for free advice on what to do next.

Call Us: Our Homeowner Ally Team is highly trained to be able to answer all your loss mitigation related questions. Our homeowner facing team members receive 220+ hours of training a year, including daily and weekly huddles to get the most up-to-date information when new policies and programs are released. Your Homeowner Ally will work with you to answer a series of questions that will help you evaluate the best option for your unique situation.

NEW! Would you rather self-service? If so, you can use our new online loss mitigation eligibility tool. You will be presented with a series of questions to help evaluate you for the workout option that best fits your need. You will have the option to go back and select alternative answers if you are presented with an option you believe does not meet your expectations. And of course, if you have questions, give your Homeowner Ally a call.

Visit our "Mortgage Assistance” FAQs for details on how to contact a HUD-approved housing counselor for free and other government-approved resources such as the CFPB’s forbearance assistance website.

What is a Homeowner Ally and how do I know who mine is?

At RANLife Home Loans, the Homeowner Ally Department is synonymous with the Loss Mitigation Department. Once you submit an application for loss mitigation, you will be assigned a Homeowner Ally, or single point of contact, to assist you through the loss mitigation process. You will receive a Homeowner Ally assignment letter from us that lets you know the name and direct contact information for your Ally. For the time your loan is in loss mitigation status, every time you call us, or we call you, you’ll get the same real, live person to talk to who knows you and understands your unique situation.

What is loss mitigation and how do I apply?

How do I avoid mortgage assistance scams?

Unfortunately, scammers are out there in times like this. What you should know is that we will never ever ask you for your personal information in an email or text message. If we reach out to you, we won’t ask for confidential information, such as your password, personal identification number (PIN) or other account information. We encourage you to be aware of loss mitigation and foreclosure rescue scams. If you see or hear something that doesn’t seem right, please contact us directly to inquire.

What should I do if I’m unsure if an inquiry is legitimate from my mortgage servicer?

If you receive a suspicious call, text message, email, or mailing claiming to be from RANLife Home Loans, and you have any doubt about the legitimacy of the contact, please hang up immediately and call the Homeowner Care number on your Homeowner Website page, or the number noted on your monthly statement.

What can I do to protect myself from fraud?

Never give out personal information, debit or credit card numbers, or wire money or send gift cards as a result of an unexpected or unsolicited call if you cannot validate the caller’s authenticity. RANLife Home Loans provides many options for payment; be suspicious if the caller is REQUIRING funds to be sent in non-traditional payment methods. Never pay a third party for help with loss mitigation or home retention assistance. Help with home retention options, including housing counseling, is FREE. Should you become suspicious, ask the caller for details about his or her name, phone number, company, etc. Your questions may scare them away. If the conversation continues, document what they tell you, including the date and time you speak with them, caller ID number and anything else that may aid in a possible investigation. Know how to access your monthly bill easily to verify our contact information. You can access your account online through your Homeowner Website at any time or call our Homeowner Care number for any questions you may have.

What red flags should I look out for to try to identify a mortgage servicing-related scam?

Scammers may use some of the following techniques to attempt to obtain funds or personal information from you. Safeguard yourself against potential scams by being aware of the following techniques:

- Pressure to send money as fast as possible/by a set deadline

- Threatened with law enforcement action

- Asked to send funds through wire transfer services

- Told to purchase gift cards and provide codes as a form of payment

- Being instructed to not trust RANLife Home Loans

- The caller exhibits irritation, unease, or anger when you question their authority. Notice if their emotion intensifies when you ask to speak with their manager, for their phone number, or to call back later

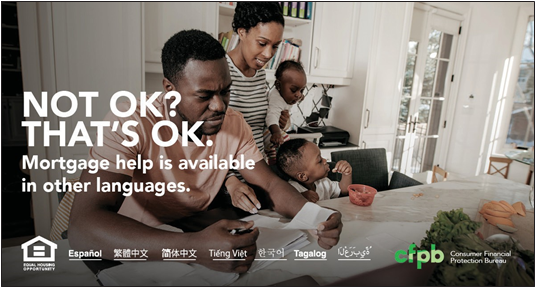

Do you have Homeowner Care agents that speak languages other than English?

We do! RANLife Home Loans has on-demand Interactive Voice Response (IVR) available over the phone en Español, and a full Homeowner Care Team of Spanish-speaking members. And for those who have a preference outside of English or Spanish, we happily offer verbal translations in more than 200 languages and regional dialects. De nada! (That’s Spanish for, "No Problem!") We also make and accept calls through the federal Telecommunications Relay Service (TRS) to accommodate homeowners with hearing or speech disabilities.

When you call our toll-free Homeowner Care Center, you’ll be presented with an option to enter a Spanish IVR by pressing 8 during the greeting message. If you choose an option to speak with a homeowner facing team member, you’ll be routed directly to someone who speaks Spanish.

If you prefer a language other than English or Spanish, just let us know and we’ll update your account and assist you through our trusted translation partners.

If you’ve designated a Spanish language preference, you’ll automatically be assigned a Spanish speaking Homeowner Ally (single point of contact) once you apply for loss mitigation.

If you’d like to self-service, you can update your language preference any time by logging into your account, selecting "Manage Your Account," "Profile Info," and then "Change" under "Preferred Language.

Help is also available in other languages at http://www.cfpb.gov/housing and through the Federal Housing Finance Agency’s (FHFA) Interpretive Services website here.

https://www.fhfa.gov/MortgageTranslations/Pages/Interpretive-Services.aspx

What other resources can you suggest for assistance?

Need Help? To find a HUD-approved housing counselor for free advice on what do to do next, call 1-800-569-4287 or visit http://www.cfpb.gov/housing for more information about forbearance.

Remember, homeowners should avoid anyone who seeks a fee in exchange for obtaining forbearance assistance. Help with home retention options, including housing counseling, is FREE.

Where can I find information about the Homeowner Assistance Fund?

The Homeowner Assistance Fund (HAF) is a federal program authorized by The American Rescue Plan Act of 2021. The purpose of the HAF is to help homeowners experiencing a financial hardship as a result of COVID-19 catch up on mortgage and utility bills and pay other housing costs. Funds from the HAF may be used for assistance with mortgage payments, homeowner’s insurance, utility payments, and other specified purposes. Each state is responsible for requesting and disbursing funds under their own HAF programs. As state programs become available, they will be listed on the National Council of State Housing Agencies (NCSHA) website. We are happy to coordinate with the State Housing Finance Agencies on getting our homeowners back on track.

Learn more about the program at www.consumerfinance.gov/haf or by calling (800) 569-4287.

Obtenga más información sobre el programa en www.consumerfinance.gov/haf o llamando al (800) 569-4287.

What is the Homeowner Assistance Fund (HAF)?

The Homeowner Assistance Fund (HAF) is a federal assistance program that helps homeowners who have been financially impacted by COVID-19 pay their mortgage or other home expenses. The HAF program available to you will depend on your area. Each state or territory developed its own program. Programs were also developed by Tribes (or their Tribally Designated Housing Entity), the Department of Hawaiian Home Lands, and the District of Columbia.

Am I Eligible?

To be eligible, you must:

- Have experienced a financial hardship associated with the COVID-19 pandemic.

- Apply for assistance for your primary residence.

- Have household income at or below your state’s program requirements. Most state programs limit eligibility to households with less than 150% of the median income in your area or $79,900, whichever is higher. Some programs have established lower limits, so check your program’s income requirements before applying.

- Meet additional requirements specific to the program where you are applying.

How Do I Apply?

Visit www.consumerfinance.gov/haf to check your local program. Application processes may vary by location. You will need to verify that you meet income requirements and may need to provide additional necessary documentation.

Questions?

For any other questions, see www.consumerfinance.gov/haf/ or contact a HUD-approved housing counseling agency at www.consumerfinance.gov/find-a-housing-counselor or (800) 569-4287. They can help guide you through the application process.

Additional Resources:

Avoid Foreclosure:

Exit Forbearance:

Help for Homeowners:

https://www.consumerfinance.gov/coronavirus/mortgage-and-housing-assistance/help-for-homeowners/

Help for American Indian, Alaska Native, and Native Hawaiian People:

¿Soy Eligible Para Participar?

Para ser elegible, usted debe:

Haber experimentado dificultades financieras asociadas con la pandemia del COVID-19.

Solicitar ayuda para su residencia principal.

Tener un ingreso familiar igual o inferior a los requisitos del programa de su área. La mayoría de los programas limitan la elegibilidad a los hogares con menos del 150% del ingreso medio en el área o $79,900, lo que sea más alto. Algunos programas han establecido límites más bajos, así que verifique los requisitos de ingresos de su programa antes de presentar la solicitud (en inglés).

Es posible que también tenga que cumplir requisitos adicionales específicos del programa al que solicita.

¿CÓMO PRESENTO UNA SOLICITUD?

Visite www.consumerfinance.gov/haf/ a consulte su programa local. Los procesos de solicitud pueden variar según la ubicación. Usted deberá comprobar que cumple con los requisitos de ingresos y es posible que tenga que proporcionar documentación adicional necesaria.

¿PREGUNTAS?

Para cualquier otra pregunta, visite www.consumerfinance.gov/haf/ o póngase en contacto con una agencia de asesoramiento en materia de vivienda aprobada por el Departamento de Vivienda y Desarrollo Urbano de Estados Unidos (HUD, por sus siglas in inglés) a www.consumerfinance.gov/find-a-housing-counselor o (800) 569-4287.

Recursos adicionales:

Evite la ejecución hipotecaria:

Salga del Aplazamiento:

Asistencia para propietarios de viviendas:

https://www.consumerfinance.gov/coronavirus/mortgage-and-housing-assistance/help-for-homeowners/

Ayuda para indígenas americanos, nativos de Alaska y nativos de Hawái (disponible solo en inglés):